Article II 5/2024: THE EUROPEAN UNION: CURRENT TUNA PRODUCTION, MARKET AND UPCOMING REGULATORY CHALLENGES

By Roberto Alonso, Secretary General of ANFACO-CECOPESCA

Canned tuna production in the European Union is about 400 000 tonnes per year, and the per capita yearly consumption is around 1.3 kg. Of great relevance to producers and exporters of canned tuna to this important market is the evolving regulatory landscape which will come into force within the next few years, adding on to the already stringent rules for access. This article highlights some of the upcoming developments; it also calls upon all stakeholders to revitalise efforts to promote the health benefits of tuna in the face of challenges such as plant-based foods.

Production of prepared and preserved fishery products in 2022 exceeded 1.14 million tonnes in the European Union (Eurostat.Prodcom). Of the total, tuna and bonito products accounted for approximately 35%, which works out to about 400 000 tonnes of prepared and preserved product per year. The production of canned tuna is the main contributor to these figures.

Canned tuna trade and market flows

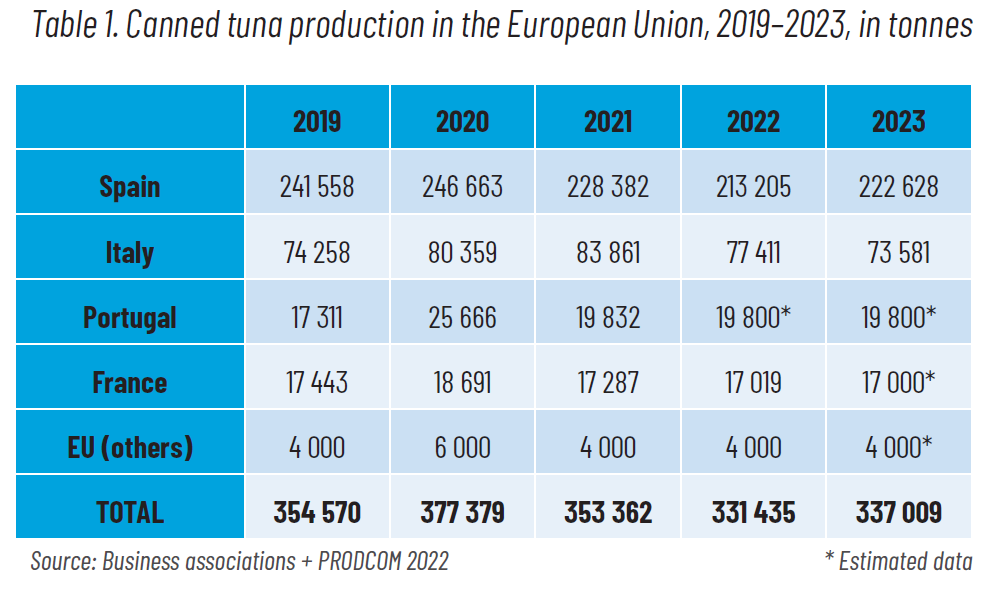

Table 1 shows the production trend for canned tuna production in the European Union from 2019 to 2023. Spain contributes about two-thirds of the total, which in 2023, amounted to 222 628 tonnes.

The data for 2023 shows an upward trend of +1.6% compared to 2022, reflecting a recovery following the slowdown suffered as a result of the COVID-19 pandemic. Growth is expected to stabilise in 2024.

The data for 2023 shows an upward trend of +1.6% compared to 2022, reflecting a recovery following the slowdown suffered as a result of the COVID-19 pandemic. Growth is expected to stabilise in 2024.

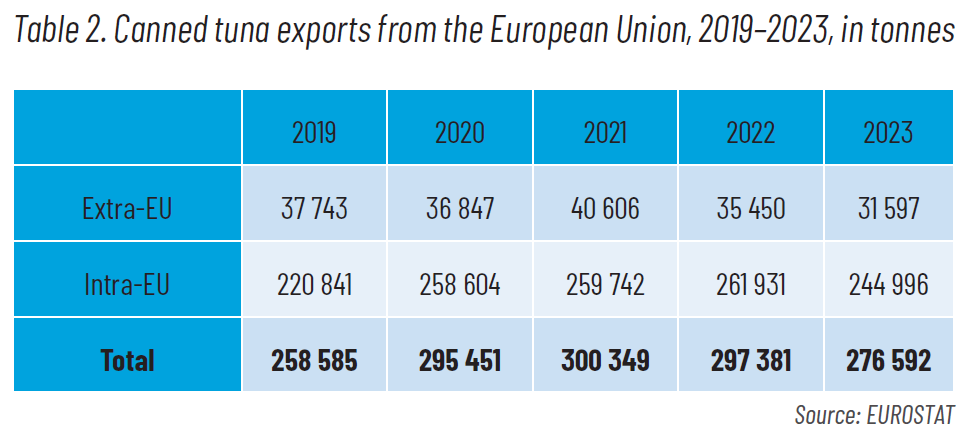

To understand the evolution of European canned tuna production, the export-import flows must be studied, as well as EU domestic consumption. In 2023, EU exports amounted to 276 592 tonnes, +7% compared to 2019 (Table 2). Of this, 89% constituted intra-EU trade. A review of the historical data indicates that there has been a strengthening of canned tuna exports from the EU after the pandemic. Outside the European Union, the first export destination is the United Kingdom.

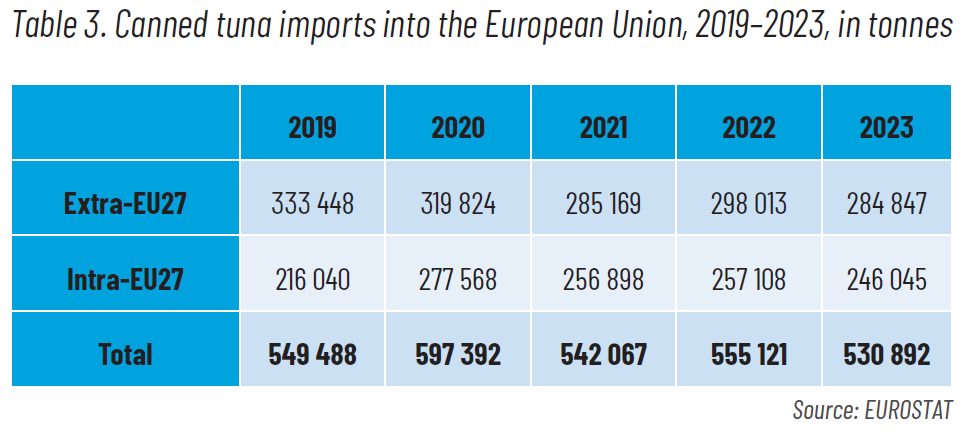

On the contrary, EU imports have dropped in the past few years. In 2023, imports amounted to 530 892 tonnes, representing a drop of 3.4% compared to 2019; of this, 54% (specifically 284 847 tonnes) came from countries outside the European Union. Table 3 shows a declining trend in the exports of foreign suppliers to the European Union, which should be analysed on a case-by-case basis at the end of 2024, in terms of raw material availability, geopolitical context or business changes. It is important to highlight changes in the supplying trends from countries such as Ecuador, Seychelles, Philippines, Mauritius, Papua New Guinea or Côte d’Ivoire.

It is possible that after COVID-19, the European industry itself has strengthened its position in the domestic market, thanks to the reliability and quality of its products. This observation does not consider the economic value of production which, due to international inflation, is subject to market adjustments.

At the same time, domestic consumption of canned tuna in the European Union is affected by inflation (apart from 2020, when apparent consumption exceeded 660 000 tonnes during the pandemic). Thus, for 2022, it was estimated that 589 175 tonnes were bought by consumers, down by 8.7% compared to 2019. European per capita yearly consumption is around 1.3 kg, with a negative projection for 2023, but a recovery is expected in 2024. In terms of the total quality consumed, the main countries continue to be Spain, Italy and France, while Malta has the highest per capita consumption with 3.4 kg/inhabitant/year. In order to satisfy the EU canned tuna market in 2023, this would require more than one million tonnes of whole (round) tuna as raw material.

At the same time, domestic consumption of canned tuna in the European Union is affected by inflation (apart from 2020, when apparent consumption exceeded 660 000 tonnes during the pandemic). Thus, for 2022, it was estimated that 589 175 tonnes were bought by consumers, down by 8.7% compared to 2019. European per capita yearly consumption is around 1.3 kg, with a negative projection for 2023, but a recovery is expected in 2024. In terms of the total quality consumed, the main countries continue to be Spain, Italy and France, while Malta has the highest per capita consumption with 3.4 kg/inhabitant/year. In order to satisfy the EU canned tuna market in 2023, this would require more than one million tonnes of whole (round) tuna as raw material.

Frozen/thawed preparations

A new consumer niche market for tuna is emerging in Europe, consisting of frozen or defrosted sliced product. This raw material must come from vessels that have frozen the tuna down to -18°C according to EU Regulation 853/2004. The market volume for this product is estimated at 68 000 tonnes per year, two-thirds of which are marketed through the hotel, restaurant and catering (HORECA) channel and the remainder at retail level.

This new market segment requires approximately 150 000 tonnes of whole (round) tuna per year.

This new market segment requires approximately 150 000 tonnes of whole (round) tuna per year.

Changes in post-COVID consumption

Given the previous data, it is worth asking what is happening with the European consumer. A survey carried out by Mintel for the European consumer and the United Kingdom in 2022, asked about the main barriers to fish consumption. The main finding was that “it is too expensive”.

Let me share a thought. It is clear that a willingness to pay for tuna products means that the consumer perceives that he or she is getting more value than he/she is paying for. And if inflation pushes prices up, strategies must focus on innovation with the aim of further improving the consumer’s perception over the product.

Of all the marketing strategies, tuna has one big ally: health. Precise communication about the health benefits of eating tuna can help to increase consumption in the European Union. Therefore, the global industry must make a collective effort to reinforce messages in this direction, incorporating the importance and benefit, for example, of selenium in its interaction in the diet in the face of exposure to mercury present in tuna; or the need to ingest Omega-3 fatty acids. It is essential to activate public debate, highlighting the positive aspects of eating tuna for health because the growth of the market depends on it, at least in the European Union.

The latest European Market Observatory for fisheries and aquaculture products (EUMOFA) study shows that, in 2022, households in countries such as Italy, Spain and France used more than two-thirds of their total expenditure on meat products. In other words, fish, such as tuna, have the capacity to absorb part of this expenditure with well-targeted promotional strategies, which must also consider the reputational and sustainability aspects. In that sense, there are eco-labelling strategies already put in place, and the EU’s “Green Claims Directive” will help to protect consumers from “greenwashing” practices. The positive message is, there is opportunity to grow if we do it right.

Let me share a thought. It is clear that a willingness to pay for tuna products means that the consumer perceives that he or she is getting more value than he/she is paying for. And if inflation pushes prices up, strategies must focus on innovation with the aim of further improving the consumer’s perception over the product.

Of all the marketing strategies, tuna has one big ally: health. Precise communication about the health benefits of eating tuna can help to increase consumption in the European Union. Therefore, the global industry must make a collective effort to reinforce messages in this direction, incorporating the importance and benefit, for example, of selenium in its interaction in the diet in the face of exposure to mercury present in tuna; or the need to ingest Omega-3 fatty acids. It is essential to activate public debate, highlighting the positive aspects of eating tuna for health because the growth of the market depends on it, at least in the European Union.

The latest European Market Observatory for fisheries and aquaculture products (EUMOFA) study shows that, in 2022, households in countries such as Italy, Spain and France used more than two-thirds of their total expenditure on meat products. In other words, fish, such as tuna, have the capacity to absorb part of this expenditure with well-targeted promotional strategies, which must also consider the reputational and sustainability aspects. In that sense, there are eco-labelling strategies already put in place, and the EU’s “Green Claims Directive” will help to protect consumers from “greenwashing” practices. The positive message is, there is opportunity to grow if we do it right.

But action needs to be taken through extensive promotion campaigns. If not, the rise of vegan substitute products, which seek to imitate canned tuna through the use of unfair comparative advertising labels and slogans such as “better”, “healthier” and “environmentally friendly”, may impact upon tuna and other fish. As a business association dating back to 1904, ANFACO-CECOPESCA is working to defend the tuna industry under Article 36 of EU Regulation 1169/2011.

Upcoming legislative changes in Europe

In the next few years, new legislation will come into force in Europe that will modify supply and marketing chains, resulting in a big impact on the tuna industry. Within the next three years, the prohibition of products made with forced labour will come into being, which means that any Member State or the European Commission itself will have the capacity to investigate entire supply chains and act accordingly. Also, a revised Fisheries Control Regulation will impose digital/electronic traceability requirements under Chapter 3 for value chain tuna, i.e. frozen, smoked or salted, within two years, in parallel with the entry into force of CATCH IT, the EU’s digital catch certificate. In addition, for Chapter 16 products like canned tuna, the European Commission will carry out a study with a view to implementing traceability changes by 2029.

The European Commission in Brussels is therefore exhibiting firm purpose to ensure compliance in creating a level playing field in the European market; and speeding up internal decision-making processes such as the imposition of yellow cards for illegal, unreported and unregulated (IUU) fishing, among others.

But that’s not all: in terms of sanitary standards, changes are coming for the Bisphenol-A (BPA) content in metal packaging; new MOAH (Mineral Oil Aromatic Hydrocarbons) limits will affect the vegetable oils used; and a new European packaging and packaging waste regulation will impose stricter requirements for plastics used as packaging materials.

Finally, a revision is underway of the European Regulation 853/2004 for vessels freezing tuna at -18°C, in terms of new validation requirements, temperature charts and additional traceability requirements.

All these changes should be expected, with the aim of continuous improvement of standards, and better practices.

The European Commission in Brussels is therefore exhibiting firm purpose to ensure compliance in creating a level playing field in the European market; and speeding up internal decision-making processes such as the imposition of yellow cards for illegal, unreported and unregulated (IUU) fishing, among others.

But that’s not all: in terms of sanitary standards, changes are coming for the Bisphenol-A (BPA) content in metal packaging; new MOAH (Mineral Oil Aromatic Hydrocarbons) limits will affect the vegetable oils used; and a new European packaging and packaging waste regulation will impose stricter requirements for plastics used as packaging materials.

Finally, a revision is underway of the European Regulation 853/2004 for vessels freezing tuna at -18°C, in terms of new validation requirements, temperature charts and additional traceability requirements.

All these changes should be expected, with the aim of continuous improvement of standards, and better practices.

ADVERTISEMENTS